We believe everyone should be able to make financial decisions with

confidence. While we don't cover every company or financial product on

the market, we work hard to share a wide range of offers and objective

editorial perspectives.

So how do we make money? Our partners compensate us for advertisements that

appear on our site. This compensation helps us provide tools and services -

like free credit score access and monitoring. With the exception of

mortgage, home equity and other home-lending products or services, partner

compensation is one of several factors that may affect which products we

highlight and where they appear on our site. Other factors include your

credit profile, product availability and proprietary website methodologies.

However, these factors do not influence our editors' opinions or ratings, which are based on independent research and analysis. Our partners cannot

pay us to guarantee favorable reviews. Here is a list of our partners.

Does Applying For a New Credit Card Hurt Your Credit?

A new credit card application triggers a hard inquiry that temporarily drops your credit score — but the new line of credit can help your score in the long run. Learn more about the pros and cons of opening a new card.

Many, or all, of the products featured on this page are from our advertising

partners who compensate us when you take certain actions on our website or

click to take an action on their website. However, this does not influence our

evaluations. Our opinions are our own. Here is a list of our partners and

here's how we make money.

Updated · 3 min read

How is this page expert verified?

NerdWallet's content is fact-checked for accuracy, timeliness and

relevance. It undergoes a thorough review process involving writers and

editors to ensure the information is as clear and complete as possible.

Lauren Schwahn is a writer at NerdWallet who covers credit scoring, debt, budgeting and money-saving strategies. She contributed to the "Millennial Money" column for The Associated Press and managed a team of writers producing content for the series. Her work has also been featured by USA Today, MSN, The Washington Post and more. Lauren has a bachelor’s degree in history from the University of California, Santa Cruz. She is based in San Francisco.

Sheri Gordon is a former assigning editor on the Core Personal Finance team at NerdWallet and has edited financial content for more than 20 years. Before joining NerdWallet, Sheri was on the business and metro copy desks at the Los Angeles Times, where she worked on stories that won the 1998 Pulitzer Prize for breaking news. Sheri has edited publications on arts, culture, food, education and activism. She has also edited books on water policy, healthy living and architecture. Sheri earned a Bachelor of Arts in history at the University of California, Los Angeles.

Bev O'Shea is a former NerdWallet authority on consumer credit, scams and identity theft. She holds a bachelor's degree in journalism from Auburn University and a master's in education from Georgia State University. Before coming to NerdWallet, she worked for daily newspapers, MSN Money and Credit.com. Her work has appeared in The New York Times, The Washington Post, the Los Angeles Times, MarketWatch, USA Today, MSN Money and elsewhere. Twitter: @BeverlyOShea.

personal finance writer

SOME CARD INFO MAY BE OUTDATED

This page includes information about these cards, currently unavailable on

NerdWallet. The information has been collected by NerdWallet and has not

been provided or reviewed by the card issuer.

Yes, it true — opening, or simply applying for, a new credit card can cause a brief drop to your credit score. That’s because when you apply, the lender checks your credit report to decide whether to approve you. This check is called a hard inquiry (or “hard pull”) and its effects on your credit are temporary.

But getting a new card can also come with a few advantages for your credit, such as raising your available credit. Here’s what to know.

Does applying for a credit card hurt your credit?

Yes. When a card issuer looks at your credit information because you’ve applied for a credit card, it is a hard inquiry. This peek into your credit file by the lender can lead to a slight drop in your credit score, whether you are approved or not.

A new inquiry typically takes less than five points off your FICO scores, according to FICO. The stronger your credit score, the less likely your score will be impacted by a credit application.

The impact of hard inquiry on your credit score fades over time — likely after six months — while the record of the inquiry remains on your credit reports for two years.

To review which lenders have made hard or soft inquiries into your credit file, request your free weekly credit reports from AnnualCreditReport.com or directly from the three major credit bureaus: Experian, Equifax and TransUnion.

Stress less. Track more.

See the full picture: savings, debt, investments and more. Smarter money moves start in our app.

Why does applying for a credit card hurt your score?

Hard inquiries on your credit file show that you’re seeking new credit. These inquiries are interpreted by FICO and VantageScore as a sign that you might be in financial distress or engaging in risky behavior. The small point penalty to your score reflects that view.

Your score can drop more if you apply for several cards or loans in a short time. To protect your score, try to space out applications — NerdWallet suggests waiting about six months between them.

Before you apply for a credit card

Consider these factors:

Whether your application is approved or rejected makes no difference in your score. That’s why it makes sense to be almost certain you will qualify before you apply. You don’t want to lose points and still not have the credit you needed.

Applications can affect people’s credit differently. For example, an applicant with a high credit score and a long history of on-time payments is unlikely to lose as many points as someone with a lower score and a shorter, imperfect track record.

Points lost as a result of credit applications are likely to return in about six months. So if you are planning to apply for a loan for, say, a car or home, it’s a good idea not to apply for any other credit for at least six months before that loan’s final approval.

Pros and Cons of opening a new credit card

Opening a new credit card isn’t all good or bad for your credit score — it depends on how you use it. Here are the key pros and cons to weigh before you apply.

Pros

Build credit through on-time payments, added available credit and responsible use.

Increase available credit that lowers your utilization ratio.

Improve credit mix or adds variety if you only have loans or a few accounts.

Earn rewards like access to cash back, points or travel perks.

Cons

Temporary dip in credit score due to hard inquiry.

Shorter credit history, because the new account lowers the average age of your accounts.

Temptation to overspend, which can lead to unmanageable debt.

Higher interest costs if you carry a balance month-to-month.

Annual fees, if you apply for a credit card.

How opening a new card can help your credit

It can give you a better track record

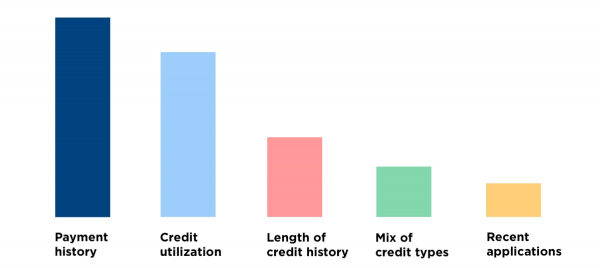

Paying on time, every time is essential for good credit. Payment history accounts for 35% of FICO credit scores, the ones most commonly used in credit decisions. Competitor VantageScore says it makes up 40% of your 3.0 score.

If you’re trying to build credit, nothing is more important than consistent, on-time payments. A new account gives you another opportunity to build up a record of on-time payments.

It gives you more room on credit cards

A new card will increase your overall credit limit. If your spending stays the same, your overall credit utilization will be lower, and that could help your score.

It can create credit diversity

Credit scores award points for showing you can manage more than one type of credit. If you have an installment loan but do not have an existing credit card, successfully managing your new credit card is likely to help. But if you already have several credit cards, adding one more is not as likely to have much of an impact.

Stress less. Track more.

See the full picture: savings, debt, investments and more. Smarter money moves start in our app.

How opening a new credit card can hurt your credit

It can lead to higher balances

Your score can drop if you use too much of your newly available credit. This causes your credit utilization to spike, and that's an important credit scoring factor. Experts recommend going no higher than 30% on any card, and lower is better.

It may lower the average age of your accounts

Getting a new card can also negatively impact your score if you have a limited credit history. Because a big part of your credit score is how long you’ve had credit, a new account lowers your average account age, which can cause a drop to your score.

Length of credit history makes up 15% of your FICO score. VantageScore weights “depth of credit” more heavily — 21% — making it the second most important factor in your VantageScore 3.0 calculation.

Want to try out a few scenarios about applying for credit and how it might affect your score? As part of NerdWallet’s free credit score tool, you can use the credit score simulator to estimate the effect of various actions.

🤓Nerdy Tip

When you apply for a credit product that involves a hard inquiry on your credit, you may get an influx of marketing messages from lenders. This happens because credit bureaus sell marketing lists triggered by hard inquiries. But you can opt out, either permanently or for five years. Visit OptOutPreScreen, a service of credit bureaus Equifax, Experian, TransUnion and Innovis, or call 888-567-8688. The bureaus say your request will be effective within five days. Note that you may still receive marketing offers from lenders that use other sources. Opting out does not affect your credit score or your ability to apply for credit or insurance.

Article sources Article sources

NerdWallet writers are subject matter authorities who use primary,

trustworthy sources to inform their work, including peer-reviewed

studies, government websites, academic research and interviews with

industry experts. All content is fact-checked for accuracy, timeliness

and relevance. You can learn more about NerdWallet's high

standards for journalism by reading our

editorial guidelines.