Although qualifying can be difficult, banks remain the most common source of financing for small businesses — compared with options such as online lenders, community financial institutions and credit unions.

Bank loans for businesses offer low interest rates, long repayment terms and can be used for a variety of purposes. The right bank for you should offer the loan you need, as well as fund enough loans to make financing possible.

We reviewed the best banks for small-business loans based on their commercial and industrial lending volume, product offerings and qualifications, among other features.

Open to loans from sources other than traditional banks? See our roundup of the best small-business loans across all lender types.

Why trust NerdWallet

Why trust NerdWallet

250+ small-business products reviewed and rated by our team of experts.

80+ years of combined experience covering small business and personal finance.

50+ categories of the best business loan selections.

Objective and comprehensive business loans ratings rubric. (Learn more about our star ratings.)

NerdWallet's small-business loans content, including ratings, recommendations and reviews, is overseen by a team of writers and editors who specialize in business lending. Their work has appeared in The Associated Press, The Washington Post, MarketWatch, Nasdaq, Entrepreneur, ABC News, MSN and other national and local media outlets. Each writer and editor follows NerdWallet's strict guidelines for editorial integrity to ensure accuracy and fairness in our coverage.

How much do you need?

We'll start with a brief questionnaire to better understand the unique needs of your business. Once we uncover your personalized matches, our team will consult you on the process moving forward.

Best banks for business loans

Click on a provider to jump to details about its business loan offerings, or keep reading to learn about how to get business financing from banks, as well as alternative funding options.

Compare the best banks for business loans

Bank | Best for | Loan amounts | Branch locations |

|---|---|---|---|

Customer relationships and loyalty programs. | $1,000 - $5 million | All U.S. states. | |

Variety of small-business products. | $5,000 - $5 million | All U.S. states, except Hawaii and Alaska. | |

SBA loans. | $5,000 - $5 million | AL, AK, AR, AZ, CA, CO, CT, DE, FL, GA, ID, IL, IA, KS, KY, MD, MN, MS, MT, NE, NV, NJ, NM, NY, NC, ND, OR, PA, SC, SD, TX, UT, VA, WA, WI and WY, plus D.C. | |

Simple options and in-person service. | $5,000 - $10 million | Six metropolitan areas: Chicago, D.C., Los Angeles, Miami, New York City, San Francisco. | |

Automatic loan payments. | $10,000 - $5 million | AL, AZ, CA, CO, DE, FL, GA, IL, IN, KS, KY, MA, MD, MI, MO, NC, NJ, NM, NY, OH, PA, SC, TN, TX, VA, WI, WV, plus D.C. | |

Startups. | $5,000 - $5 million | AR, AZ, CA, CO, IA, ID, IL, IN, KS, KY, MN, MO, MT, NC, ND, NE, NM, NV, OH, OR, SD, TN, TX, UT, WA, WI and WY. | |

Applying online. | Up to $5 million | AL, AR, FL, GA, IN, KY, MD, MS, NC, NJ, OH, PA, SC, TN, TX, VA, WV, plus D.C. | |

Lines of credit up to $5 million. | $10,000 - $5 million | CA, GA, IL, MA, NY, PA TX, VA. | |

Fast approval. | $10,000 - $5 million | AL, FL, GA, IL, IN, KY, MI, NC, OH, SC, TN, WV. |

1. Bank of America

Best for: Customer relationships and loyalty programs.

Bank of America is the biggest commercial and industrial loan bank lender in the U.S. — according to data compiled by S&P Global in March 2025 — surpassing the next closest lender by more than $120 billion. It operates in all U.S. States.

May be a fit for: Bank of America business loans are a good choice if you value rewards and use other Bank of America or Merrill products. By meeting certain account requirements, you can qualify for interest rate discounts, no fees on wire transfers and other benefits. Bank of America may also make sense for business loans for veterans and service members, as it offers them a 25% discount on loan administration or origination fees.

Here’s what Bank of America has to offer:

Term loans

Bank of America issues both fixed-rate secured and unsecured term loans. Its secured loan requires greater annual revenue: $250000 versus $100000 for the unsecured option. But it also offers higher borrowing limits — up to $250000 — and a potentially lower interest rate. Both business loans require at least two years in business and can have repayment terms of up to five years, which is less than some other banks may offer.

Business lines of credit

Bank of America offers unsecured and secured business lines of credit, with the same revenue requirements as its term loans ($100000 and $250000, respectively). The secured line of credit comes with additional borrowing power — starting at $25,000 compared with $10,000 for the unsecured option. Borrowing maximums are not disclosed. Both have revolving terms, meaning you use the money as needed, that renew annually.

For newer businesses (those with at least 6 months in operation and $50000 in annualized revenue), Bank of America offers a cash secured business line of credit. With this product, you must provide a security deposit to match your credit line limit with minimum initial deposits starting at $1000. You can then use the line of credit to cover daily expenses, make regular payments and establish a positive account history — with the goal to transition to an unsecured business line of credit.

SBA loans

Bank of America is a preferred Small Business Administration lender, but other banks on this list are more active in issuing SBA loans. For example, U.S. Bank and Wells Fargo have approved a higher number of 7(a) loans — the most common type of SBA funding — so far in the SBA’s 2026 fiscal year (which started on Oct. 1, 2025).

Other business loans

Bank of America offers business auto loans starting at $10,000, as well as commercial real estate loans and equipment loans, which both start at $25,000. The lender also administers a specialized program for medical practice loans.

Read our full review of Bank of America business loans.

2. JP Morgan Chase

Best for: Variety of small-business products.

Chase ranks as the second-largest U.S. bank by commercial loan amount. It operates in 48 U.S. states, but doesn’t offer business loans in Hawaii and Alaska.

May be a fit for: Chase business loans are a good option for business owners who want access to a range of business products, including small-business loans, lines of credit and commercial real estate loans, as well as business banking, credit cards and payment solutions from a single provider. With loan amounts ranging from $5,000 to $5 million, it offers financing that can grow as your business grows.

Chase business loans include:

Term loans

Chase offers fixed-rate and adjustable-rate term loans starting at $5,000 — which is a smaller starting amount than lenders like Bank of America or PNC Bank — and repayment terms that can last up to seven years. Some small-business loans have amounts as high as $500,000 with no origination fee. However, a prepayment fee may apply for loans greater than $250,000 that are paid off early.

Business lines of credit

Chase has business and commercial lines of credit. Its business line of credit provides $10000 to $500000 in funding on a renewable five-year revolving term. The commercial line can provide more than $500,000, with one- to two-year terms that may be renewed.

SBA loans

Chase is an SBA preferred lender and has approved more than 500 SBA 7(a) loans totaling over $140 million so far in fiscal year 2026. Loan amounts up to $5 million are available.

Chase funds multiple types of SBA loans, including SBA Express loans and credit lines, which offer faster funding of up to $500,000.

Other business loans

Chase offers commercial real estate loans with fixed or variable rates that start at $50,000. Terms are available for up to 25 years. Chase also gives you the option to pay back the loan on a standard repayment schedule — or make interest-only payments for a set period with a large payment at the end of the term.

Read our full Chase business loans review.

3. Wells Fargo

Best for: SBA loans.

Wells Fargo comes in third when ranked on commercial and industrial loans and offers a variety of small-business loans. It operates in 36 states plus Washington, D.C.

May be a fit for: Wells Fargo is a solid option for those interested in SBA financing. It partners with the SBA to offer both SBA 7(a) and 504 loans. (Just keep in mind that there are many other options for SBA loans.) And if an SBA loan isn’t the right fit, Wells Fargo can help you explore a number of other types of lines of credit and business loans. However, some term loan programs have been discontinued so you may want to consider other options if a term loan is what you want.

Here are Wells Fargo's business loan offerings:

Business lines of credit

Wells Fargo has two lines of credit — one unsecured and one secured by collateral — ranging from $10000 to $3000000. Credit lines of up to $150,000 are revolving with automatic enrollment in a free rewards program. You’ll typically need at least $2 million to $10 million in annual sales to qualify for Wells Fargo’s most generous business line of credit. This line of credit has either a one-year term or three-year term, depending on your borrowing amount. Fees vary by product.

SBA loans

Wells Fargo is a preferred SBA loan lender. In the 2026 fiscal year, so far, the bank has approved over 300 SBA 7(a) loans, worth more than $217 million in funding.

U.S. Small Business AdministrationSBA 7(a) loan

Max Loan Amount

$5,000,000Other business loans

Wells Fargo offers semi truck financing, equipment financing and commercial real estate purchase loans, as well as medical practice financing.

Read our full Wells Fargo business loans review.

4. Citibank

Best for: Simple options and in-person service.

Although Citibank is the fourth-largest bank in the U.S. based on commercial loan volume, it offers fewer business loan products than some other banks. Its branches are concentrated in six metropolitan areas: Chicago, Los Angeles, Miami, New York, San Francisco and Washington, D.C.

May be a fit for: The in-person, hands-on loan application experience offered by Citi might be the right option for business owners who feel developing a relationship with their banker today will offer benefits down the road. Whereas many banks offer at least some type of online application option, you can only apply for a business loan from Citi by visiting a branch location.

Here are Citi’s loan options:

Term loans

Citibank’s term loan ranges from $10,000 to $5 million. Interest rates are fixed, terms last up to seven years and loans require a personal guarantee. Citi doesn't offer a specific equipment loan, but term loans can be used for this purpose.

Business lines of credit

Citibank offers a business line of credit, with amounts ranging from $10,000 to $5 million. It comes with variable interest rates and revolving terms and requires a personal guarantee.

SBA loans

Citi is an SBA preferred lender and issues SBA 7(a) loans (up to $5 million), 504 loans (up to $10 million) and Express loans (up to $500,000) to finance working capital and equipment, inventory, commercial real estate and other purchases.

Other business loans

Citi provides a credit program that caters to minority-, women-, and veteran-owned small businesses, with loan amounts between $5,000 and $250,000. The bank also offers commercial mortgage loans, ranging from $250,000 to $10 million.

5. PNC Bank

Best for: Automatic loan payments.

PNC Bank ranks fifth among U.S. banks with regard to commercial loan volume. It operates branches in 27 states — Alabama, Arizona, California, Colorado, Delaware, Florida, Georgia, Illinois, Indiana, Kansas, Kentucky, Maryland, Massachusetts, Michigan, Missouri, New Jersey, New Mexico, New York, North Carolina, Ohio, Pennsylvania, South Carolina, Tennessee, Texas, Virginia, West Virginia and Wisconsin — as well as Washington, D.C.

May be a fit for: PNC Bank is a good choice for business owners who prefer automatic loan payments as well as mobile banking and cash flow tools. Whether you have a business term loan, line of credit or specialized financing for a vehicle, payments can automatically be deducted from your PNC business checking account.

PNC business loans include:

Term loans

PNC offers $10,000 to $100,000 for unsecured term loans and $100,001 and above for loans secured by collateral. Unsecured loans come with a fixed interest rate and terms of up to five years, whereas rates on secured loans can be fixed or variable and terms can last up to seven years.

Business lines of credit

The amounts for PNC’s lines of credit mirror the bank’s term loans, with unsecured options ranging from $10000 to $100000 and secured options of $100,001 and up. Both have variable interest rates and revolving terms. The unsecured line has an annual fee of $175, while the secured credit line charges 0.25% of the committed line amount.

SBA loans

PNC is a preferred SBA lender, but the bank is less active than some others issuing these loans. In fiscal year 2026 so far, PNC has approved just over 100 SBA 7(a) loans, compared with U.S. Bank which has approved over 1,700.

Other business loans

PNC business auto loans range from $10,000 to $250,000 with repayment terms up to six years. The bank’s commercial real estate loans come with fixed or variable interest rates, repayment terms up to 20 years (with up to a 25-year amortization) and financing amounts of $100,001 and up.

6. U.S. Bank

Best for: Startups.

U.S. Bank is ranked sixth for commercial loans. It has fewer locations than other brick-and-mortar banks, including Chase and Wells Fargo, but it still offers the variety of products you’d expect from a large lender.

May be a fit for: U.S. Bank may be a good choice for startups, as you may be able to qualify for certain products with less than a year in business. Its Quick Loan can have a minimum time in business requirement of six months, depending on the length of your relationship with the bank and the state you live in.

Here's what U.S. Bank has to offer:

Term loans

U.S. Bank offers fixed-rate, secured term loans as well as a fast business loan, which has a limit of $250,000 and a quick online application process. The Quick loan can be secured or unsecured and offers repayment terms of up to seven years. This product can be a good option for newer companies as you only need a minimum of six months in business to apply.

Business lines of credit

U.S. Bank has four business lines of credit that can be used to manage cash flow, fund major purchases and protect from overdraft charges. The bank’s revolving line of credit, called Cash Flow Manager, goes up to $250,000 and only requires a minimum of six months in business to qualify. That product has a $150 annual fee if the line of credit is less than $50,000.

SBA loans

U.S. Bank is a good choice if you’re in the market for an SBA loan. For fiscal year 2026, it has approved more than $450 million in SBA 7(a) funding.

Plus, as a preferred lender you may be able to qualify for an SBA loan from U.S. Bank with fewer than two years in business.

Other business loans

U.S. Bank offers equipment loans of up to $1 million, and soft costs of up to 25% can be included. The bank has fixed- and variable-rate commercial real estate loans with five-, 10- or 15-year repayment terms, with amortizations up to 25 years.

7. Truist Bank

Best for: Applying online.

Truist Bank is ranked seventh for commercial loans. It has branches in 16 states including Alabama, Arkansas, Florida, Georgia, Indiana, Kentucky, Maryland, North Carolina, New Jersey, Ohio, Pennsylvania, South Carolina, Tennessee, Texas, Virginia and West Virginia , along with D.C.

May be a fit for: Truist Bank is a good choice for business borrowers who want the convenience of applying for funding at a time and place of their choosing. They’ll find an online application available for various financing options up to $250,000. However, business owners who want a loan for more than that amount will have to apply for commercial financing by speaking with a bank representative or visiting a branch in person.

Here’s what Truist Bank has to offer:

Term loans

Truist offers unsecured term loans up to $50,000 with terms up to five years and with no origination fee. You can also opt for a larger loan amount, up to $100,000, but you’ll need to supply additional documentation, and you will be charged an origination fee. It’s also worth noting that Truist does offer these unsecured term loans to startups with less than two years of business history, but those loans max out at $25,000.

Business lines of credit

Truist’s unsecured business line of credit reaches up to $100,000 with up to three-year terms. Borrowers who are prepared to offer collateral, however, may be eligible for a line of credit for up to $250,000 and with up to five-year terms.

SBA loans

Truist Bank is an SBA preferred lender that participates in both the 7(a) and 504 loan programs. For fiscal year 2026, to date, Truist has approved 32 total 7(a) loans — not a big number when compared with some of the heavier hitters on this list. However, Truist’s SBA 7(a) loan amounts average around $1.7 million per loan, putting the total funding so far this fiscal year at just over $54 million.

Other business loans

Additionally, Truist offers up to 100% financing for business automobiles, commercial vehicles and equipment, as well as real estate loans for up to $250,000.

Read our full Truist business loans review.

8. Capital One

Best for: Lines of credit up to $5 million.

Capital One, which has made a name for itself in the credit card industry, also offers business financing with locations in eight states: California, Georgia, Illinois, Massachusetts, New York, Texas, Pennsylvania and Virginia.

May be a fit for: Capital One is a good option for business owners who want the ability to access a large amount of funding, but on their own timetable. Business lines of credit that top out at $5 million are offered. Also, discounted rates are available to businesses that have existing business deposit relationships with Capital One.

Capital One loan options include:

Term loans

Business loans have minimum amounts of $10,000 and maximum amounts of $5 million. Collateral or a deposit may be required to secure the loan. You have to visit a Capital One location and talk with a representative to start the application process and a business checking account is required.

Business lines of credit

Amounts for lines of credit are the same as for loans, ranging from $10000 to $5 million — one of the largest limits offered by the lenders on our list. A business checking account and visit to a Capital One location are needed to apply.

SBA loans

Capital One is an SBA preferred lender that offers 7(a), 504 and Express loans. Similar to Truist Bank, it is not a very active SBA lender based on the number of loans it funds, but its 7(a) loan amounts average over $1.1 million.

Other business loans

Capital One offers real estate loans up to $5 million with terms up to 20 years for both purchasing and refinancing. It also offers equipment financing and medical practice loans.

Read our full Capital One business loan review.

9. Fifth Third Bank

Best for: Fast approval.

Fifth Third Bank bills itself as a community bank and currently has branches in 12 states including Alabama, Florida, Georgia, Illinois, Indiana, Kentucky, Michigan, North Carolina, Ohio, South Carolina, Tennessee and West Virginia.

May be a fit for: For business entrepreneurs who want fast loan funding, Fifth Third Bank says it can approve and fund business term loans and lines of credit as quickly as one business day. And with any business loan or line of credit, the standard monthly service charge on your business checking account will be waived.

Here are loan options offered by Fifth Third Bank:

Term loans

Fifth Third Bank offers term loans with fixed interest rates, but does not disclose any other details about these products.

Business lines of credit

Both secured and unsecured lines of credit are offered. Amounts for the unsecured line of credit range from $10,000 to $100,000 and secured lines of credit are for amounts over $100,000.

SBA loans

SBA 7(a), SBA 504 and SBA Express loans are offered by the bank. While not at the top of SBA lenders, Fifth Third Bank has approved more than 250 SBA 7(a) loans for a total amount of over $217 million so far in fiscal year 2026 — more than Capital One and Citibank .

Other business loans

Fifth Third Bank also offers real estate loans and healthcare practice financing for medical, dental, optometry and veterinary practices.

Read our full Fifth Third Bank business loans review.

Can't qualify for a bank business loan?

- If you think you’ll qualify for an SBA loan, start by looking for the best SBA lenders that work for your business.

- If you are facing personal credit challenges, look for business loans for bad credit — either through online lenders, CDFIs or microlenders.

- If you need funding fast, consider these fast business loans to get capital as quickly as the same day you apply.

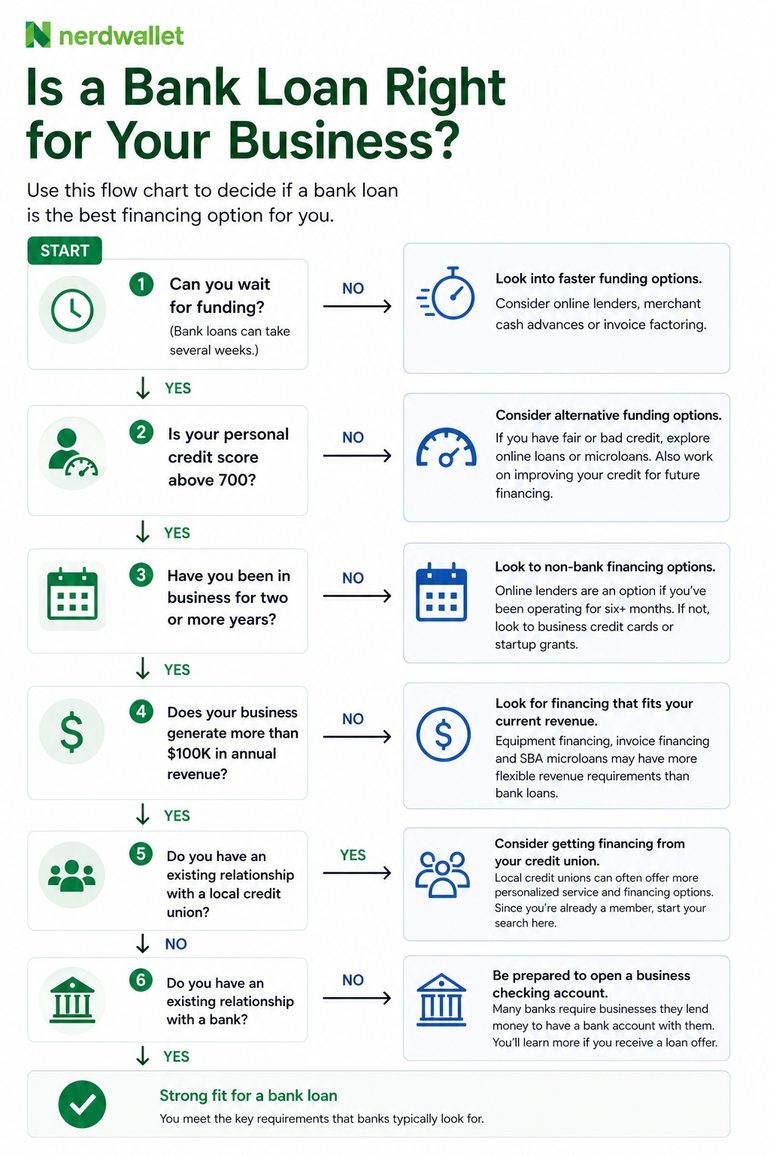

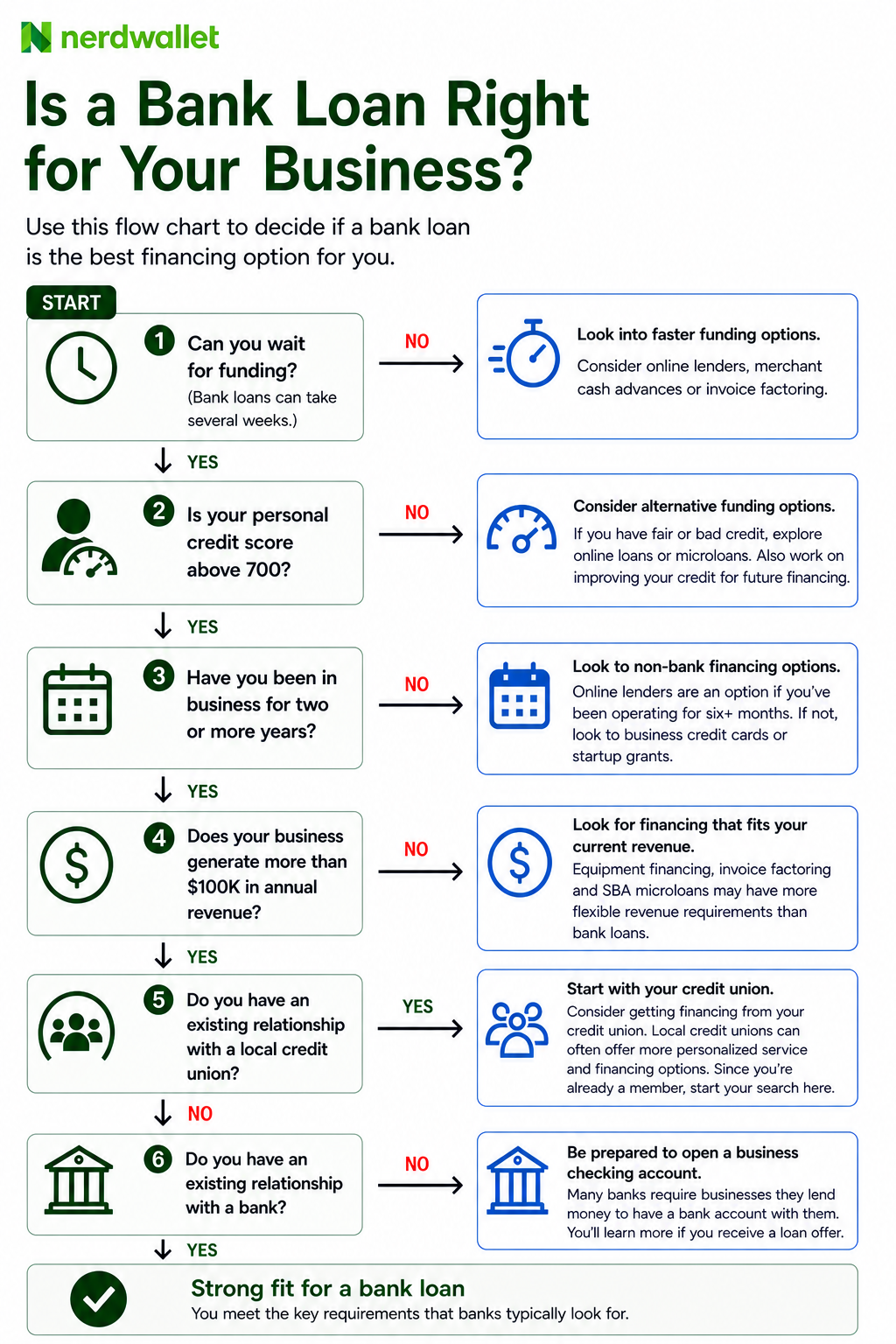

Is a business bank loan right for you?

Use our flow chart below to see if a bank loan might be a good fit for your business.

How to get a business loan from a bank

Although recent market conditions have led banks to tighten their lending standards, it’s still possible to access this type of business financing. Here’s what you need to get a business loan from a bank:

An existing relationship

Most banks require you to have at least a business checking account at their institution. While you can simply open an account at some banks to meet this qualification, you can often benefit from a longer-term relationship. For example, you need an account with Wells Fargo for at least one year to apply for financing online.

Good credit

You’ll likely need a personal credit score in the 700s — although some lenders may be a little more flexible than others. Wells Fargo, for instance, accepts a minimum credit score of 680 for its unsecured line of credit.

Potential deal-breakers in your personal credit history could include too much debt, too many open accounts or negative marks — like late payments, loan defaults and bankruptcies. The bank will check your business credit score for similar red flags.

Strong revenue

When you apply for a small-business loan, the bank will look to see whether your business is in good shape and has enough revenue to support how much you want to borrow. For example, Bank of America’s unsecured business loans require at least $100,000 in annual revenue; its secured options increase that number to $250,000.

Enough time in business

Two years under the same ownership is the standard time in business requirement. But there are exceptions. For example, some U.S. Bank lending products are available if you’ve been in business for just six months.

Collateral

You don’t necessarily need to put up business collateral like commercial property or equipment to get a bank loan for your business. Some banks offer both unsecured and secured business loans. But the bank may fund larger amounts for secured loans, while also providing longer terms and lower interest rates to make payments more affordable.

Pros and cons of bank loans for business owners

Pros

✅ Low interest rates. Business loans from banks tend to have lower interest rates than loans from non-bank lenders, helping keep the overall cost of the loan down. Currently, the average interest rate for bank loans spans 6.37% to 10.98%.

✅ Longer repayment terms. Bank loans for businesses tend to have longer repayment terms than other types of business loans, helping keep recurring payments low for borrowers.

✅ High loan amounts. Bank loans tend to have high maximum loan amounts compared with other types of business loans, helping small-business owners fund a variety of projects, such as real estate or heavy equipment purchases.

✅ Fewer surprise costs. Banks are typically more transparent with their pricing once you have a loan offer in hand compared with nonbank lenders.

Cons

❌ Difficult to qualify for. Banks usually require borrowers to jump through hoops for their loans. Common requirements include having multiple years in business, strong annual revenue and a personal credit score of 700 or higher to qualify.

❌ Slow to fund. Bank loans tend to be among the slowest types of small-business loans to fund, which can be an issue for business owners trying to cover an emergency expense or unexpected lull in cash flow.

❌ Complex application process. Applying for a business loan through a bank is typically more involved than with an online-only lender. You’ll usually need to provide more documentation, and some banks may ask you to apply in person or over the phone.

Alternatives to big bank business loans

If you can’t get a business loan from a big bank, consider these alternatives:

- Small banks and credit unions: Business loan applicants report higher approval rates from smaller banks than big-name financial institutions, as well as greater overall satisfaction, according to the Federal Reserve’s 2026 Report on Employer Firms. However, a local bank or credit union may lack the benefits you want — like online loan management or multiple locations.

- Online lenders: Online business loans come with faster funding and higher approval rates than bank loans. Some online lenders even specialize in small-business loans. For example, so far in fiscal year 2026, Newtek Bank, a digital bank, is the most active SBA 7(a) lender by loan approval count. These lenders are also less likely to require traditional collateral and may provide funding for newer businesses. But the trade-off will likely be higher costs than a traditional bank offers.

- Microlenders: Nonprofit organizations offer microloans, and these can be a good choice for startups or small businesses that need working capital but can’t qualify for a bank business loan. Microloans are typically less than $50,000 and can come with short repayment terms. Their costs may also be higher than a bank business loan.

» RELATED: 10 types of business loans

Frequently Asked Questions

What is the easiest bank to get a small-business loan?

The easiest bank to get a small-business loan will largely depend on the type of financing you need and your business’s qualifications. You might start, however, by reaching out to a bank with which you have a current relationship. Because you have an existing relationship, this bank may be more willing to help you with potential loan options.

Which banks offer startup business loans?

Some large, national banks like Bank of America, U.S. Bank and Wells Fargo offer certain loan options for companies with less than two years in business. In general, however, online and nonprofit lenders are more likely to offer startup business loans.

What are the typical requirements for a business bank loan?

To qualify for a bank loan for your business, you’ll generally need at least two years in business, a personal credit score above 700 and strong annual revenue — usually between $100,000 and $250,000 per year.

Article sources

NerdWallet writers are subject matter authorities who use primary, trustworthy sources to inform their work, including peer-reviewed studies, government websites, academic research and interviews with industry experts. All content is fact-checked for accuracy, timeliness and relevance. You can learn more about NerdWallet's high standards for journalism by reading our editorial guidelines.

- 1.FED Small Business. 2026 Report on Employer Firms: Findings from the 2025 Small Business Credit Survey. Accessed May 5, 2026.

- 2.S&P Global. Banks find 'pockets of growth' for C&I after delinquencies rise in Q4 2024. Accessed May 5, 2026.

- 3.U.S. Small Business Administration. 7(a) & 504 Lender Report. Accessed May 5, 2026.

- 2.S&P Global. Banks find 'pockets of growth' for C&I after delinquencies rise in Q4 2024. Accessed May 5, 2026.

- 3.U.S. Small Business Administration. 7(a) & 504 Lender Report. Accessed May 5, 2026.

- 3.U.S. Small Business Administration. 7(a) & 504 Lender Report. Accessed May 5, 2026.

- 3.U.S. Small Business Administration. 7(a) & 504 Lender Report. Accessed May 5, 2026.

- 3.U.S. Small Business Administration. 7(a) & 504 Lender Report. Accessed May 5, 2026.

- 3.U.S. Small Business Administration. 7(a) & 504 Lender Report. Accessed May 5, 2026.