We believe everyone should be able to make financial decisions with

confidence. While we don't cover every company or financial product on

the market, we work hard to share a wide range of offers and objective

editorial perspectives.

So how do we make money? Our partners compensate us for advertisements that

appear on our site. This compensation helps us provide tools and services -

like free credit score access and monitoring. With the exception of

mortgage, home equity and other home-lending products or services, partner

compensation is one of several factors that may affect which products we

highlight and where they appear on our site. Other factors include your

credit profile, product availability and proprietary website methodologies.

However, these factors do not influence our editors' opinions or ratings, which are based on independent research and analysis. Our partners cannot

pay us to guarantee favorable reviews. Here is a list of our partners.

Three Insurance Review 2026: A Simple but Inflexible Business Insurance Policy

Three provides broad business insurance coverage in a single policy. It’s a Berkshire Hathaway brand.

Rosalie Murphy has covered small-business banking, credit cards, insurance and lending at NerdWallet since 2021. She writes and edits the Starting Small newsletter, and her reporting has appeared in publications like the Associated Press, MarketWatch and Nasdaq. Rosalie is an MBA candidate at Kent State University and has a bachelor's degree in journalism from the University of Southern California.

Ryan Lane is an editor on NerdWallet’s small-business team. He joined NerdWallet in 2019 as a student loans writer, serving as an authority on that topic after spending more than a decade at student loan guarantor American Student Assistance. In that role, Ryan co-authored the Student Loan Ranger blog in partnership with U.S. News & World Report, as well as wrote and edited content about education financing and financial literacy for multiple online properties, e-courses and more. Ryan also previously oversaw the production of life science journals as a managing editor for publisher Cell Press. Ryan is located in Rochester, New York.

Published in

Updated

How is this page expert verified?

NerdWallet's content is fact-checked for accuracy, timeliness and

relevance. It undergoes a thorough review process involving

writers and editors to ensure the information is as clear and

complete as possible.

NerdWallet's ratings are determined by our editorial team. The scoring formula takes into account consumer complaint and customer satisfaction data.

Why trust NerdWallet

250+ small-business products reviewed and rated by our team of experts.

80+ years of combined experience covering small-business and personal finance.

Objective, comprehensive small-business insurance ratings based on the financial strength, complaint records, digital features and customer service availability of insurance market leaders. Read our methodology.

NerdWallet's small-business insurance content — including our ratings, reviews and recommendations — is produced by a team of writers and editors who specialize in small-business finances. Their journalism has appeared in The Associated Press, Washington Post, MarketWatch, Nasdaq, Entrepreneur, ABC News, MSN and other national and local media outlets. Each writer and editor follows NerdWallet's strict editorial guidelines to ensure fairness and accuracy in our coverage.

Three is one of Berkshire Hathaway’s business insurance brands. What sets Three apart is that it aims to provide all the coverage small-business owners need in one three-page policy — hence the brand name.

Three has many of the same protections you’d find in a traditional business owner’s policy, like general liability and commercial property coverage. But Three also includes commercial auto insurance, cybersecurity insurance and workers’ compensation, which most insurance companies sell as separate policies.

Simplicity is Three’s biggest selling point. The policy (which you can read here) is written in straightforward language and offers protection against a variety of different risks. It may be a good fit for business owners who want broad coverage but don’t want to buy or manage multiple policies.

The flipside is that you can’t make changes to the policy. That can make it difficult to save money on your premiums by increasing your deductible or lowering your limits — the cost is what it is. You also can’t add endorsements for other protections you might need, like property insurance coverage for your outdoor furniture.

Save up to 30% on business insurance

NerdWallet Small Business helps you get real-time quotes from 30+ insurers, and instant access to your Certificate of Insurance (COI) through our partner, Coverdash.

A single policy provides coverage that you’d normally need several insurance policies to get.

Provides some coverage that property policies normally excluded, like coverage for property damage caused by flooding.

Licensed insurance agents are available to help you shop and manage your policy.

Cons

Far more complaints about general liability and commercial property insurance filed with state regulators than we’d expect given Three’s market share.

No way to customize your policy.

Only available in 25 states as of this writing.

What Three does well

An easy way to get comprehensive coverage

Three’s policy really is innovative. It includes all the coverage types most businesses need. If you buy this policy, you won’t have to add additional coverage types later.

For instance, it automatically includes professional liability insurance, which most insurers sell separately from general liability insurance. And if you hire an employee or start using a business vehicle, you can simply add it to your policy to extend your workers’ comp or commercial auto coverage.

Good support during the purchase process

A number of online reviews say Three’s “small business advisors” — who are licensed agents — helped them understand the policy and their needs while they were buying insurance. Some online business insurance companies don’t offer any support while you’re shopping. Others only have a live chat that may or may not be staffed by a person, much less an agent.

Where Three falls short

Only available in about half of U.S. states

Three policies are not available in about half the country. Notably, businesses in Florida, New York, Washington, Massachusetts and Virginia are ineligible. Three also can’t support businesses that operate across state lines.

Shopping online for coverage in an ineligible state? Try Ergo Next, which sells policies (either its own or another company’s) nationwide.

No endorsements or modifications

Three’s simplicity has a downside: There’s little to no room to modify your policy.

Typically, when you buy insurance, you have the option to add endorsements. These fill in gaps in the standard policy. You also usually have the chance to increase your limits — which can come in handy if you have expensive equipment — or change your deductible. Three doesn’t provide those options. What’s written in the policy is what you get.

That said, Three did omit some coverage based on my answers in its quote flow (more on that below). In particular, my quote didn’t include commercial auto insurance. The price likely would have been higher if it had. So I at least wasn’t paying for coverage I didn’t need.

Want to fully customize your coverage? The Hartford offers a BOP with lots of optional add-ons.

Exclusions are unclear

It’s hard to tell whether Three’s simplicity means it does or doesn’t cover certain hazards.

For instance, business property insurance usually excludes damage caused by sinkholes or windstorms. It also usually excludes outdoor signs and property, like patio furniture. But the Three policy doesn’t outline covered causes of loss or mention outdoor signs.

In theory, if a policy doesn’t specifically exclude something, you should be covered. But if my business was in a high-risk region, like Tornado Alley, I’d want to be sure about my specific risks before buying.

I reached out to Three to find out whether their policy covers those hazards. I haven’t heard back as of this writing.

How we evaluated Three Insurance

NerdWallet’s business insurance star ratings include these factors:

Financial strength (33%). This tells us how likely an insurance company is to be able to pay out claims if there’s a major disaster or financial crisis. Three’s parent company has a “superior” rating from AM Best.

Customer complaints (33%). The National Association of Insurance Commissioners (NAIC) collects data about how many complaints were filed by an insurer’s customers. Between 2022 and 2024, Three’s parent company — Berkshire Hathaway Direct Insurance Co. — received far more complaints about general liability and commercial property insurance than we’d expect given its market share.

Purchase process (17%): Three sells its policy online, and the quote process is simple without sacrificing detail. For support, you can call a “small business advisor,” who is a licensed agent. Unfortunately, coverage is quite limited by state — about half of U.S. states aren’t available.

Customer support (17%): Few users have reviewed Three on Trustpilot and similar websites. But Three has the potential to provide good support. The phone line is open until 9 p.m. on weekdays. You can file a claim online or over the phone and request a copy of your certificate of insurance online.

I take a few additional steps when writing reviews of business insurers. These don’t currently inform our star ratings, but you’ll see details about them below:

Aggregating customer reviews and complaints. I used an AI tool to summarize what policyholders say about Three on websites like Reddit, Trustpilot and the Better Business Bureau. We don’t factor this feedback into star ratings because it’s usually anonymous and we can’t verify it. But we still think it can help shoppers understand the potential ups and downs of a particular insurer.

Trying the online quote process. If an insurer offers online quotes, as Three does, I get one. I use the same location, industry and business size information every time. The quote process can reveal how customizable policies are, hidden fees and more. We don’t include this in star ratings because many insurance companies still don’t offer online quotes, so we can’t gather the data from every brand.

Save up to 30% on business insurance

NerdWallet Small Business helps you get real-time quotes from 30+ insurers, and instant access to your Certificate of Insurance (COI) through our partner, Coverdash.

I read through online forums like Reddit and review sites like the Better Business Bureau to understand how users feel about Three. I then used an AI tool to help analyze overall sentiment. There isn’t much chatter about Three online, unfortunately. But here are the themes that stood out:

👍 Easy to get coverage

Online reviewers say Three’s digital application is quick and easy. I experienced this myself when I got a quote (more on that below). Users who called for help generally say the experience was positive and insurance agents explained things well.

👍 / 👎 All-in-one coverage

There are two sides to the all-in-one-policy coin. On one hand, users say it’s convenient to have several types of insurance covered by a single policy that only requires one premium. On the other hand, if Three drops your coverage, you’ll have to shop around for all your insurance again.

👎 Premium audits

BBB users complain that after their first year, Three performed audits and increased their premiums. This is common practice among insurance companies. But if it isn’t communicated well, it can be shocking.

It’s a good reminder to shop around before renewal for a better rate. Just know that switching insurers won't prevent audits (and bills upping your already paid premium) from heading your way.

What policies does Three Insurance sell?

Three Insurance only sells one thing — its signature three-page policy. It includes some coverage for:

Business property insurance, including coverage for theft, damage to property your business owns or rents and business interruption insurance.

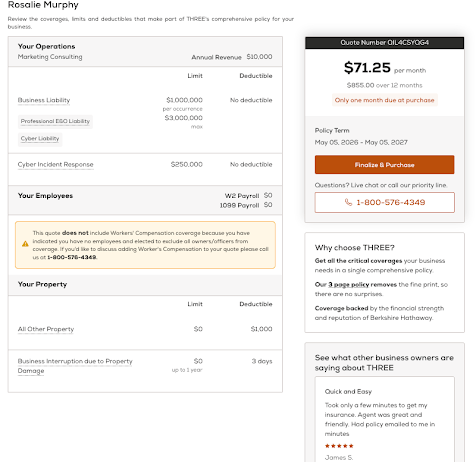

Getting an online quote from Three takes a few minutes. I went through the quote process as part of writing this review. I told Three that I was a freelance marketing consultant working out of my home, earning about $10,000 in annual revenue.

The system asked for:

My business structure and when I started it.

Where my business operates.

What I do.

My projected gross revenue for the year.

After that, it dug into some questions that hint at my liability risks:

Whether I have outside investors, employees or contractors.

Whether the business owns or leases any international locations.

If the business owns or operates aircraft, including drones, or watercraft.

If the business is responsible for a parking lot.

Additional questions asked about my professional services, like whether I always use contracts or statements of work with my clients and whether legal counsel reviews those contracts. I had to acknowledge that I don’t give advice dealing with healthcare, finance, architecture, engineering or the law.

This question seems specific to my work in marketing. When I clicked yes, it triggered an additional question: Does the business have a written procedure to check work for copyright or trademark violations? (Trademark suits are a general liability risk.)

After that, we seemed to reach the auto insurance portion of the policy. I had to say whether I transport people or goods for hire, including via rideshare or meal delivery services.

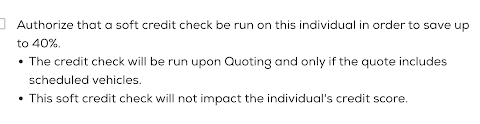

Next, the flow asked for my date of birth and address. I had the option to check the following box:

I’ve never seen an offer like this before. This may be here because Berkshire Hathaway creates credit-based insurance scores, which are common in auto insurance applications. It’s true that a soft credit pull doesn’t impact your credit score. So if your credit is in the “good” or “excellent” ranges, this may actually save you some money.

Next up: I told the quote system that my business doesn’t own or rent any property. I also excluded myself from workers’ comp coverage.

Lastly, I told Three that I don’t have any vehicles and haven’t filed any claims within the last three years. The system took about 10 seconds to generate my quote.

“Business liability” is a broad category that includes general liability, E&O, employment practices and cyber liability coverage. “Cyber incident response” pays to investigate after a data breach and cover any related liability claims.

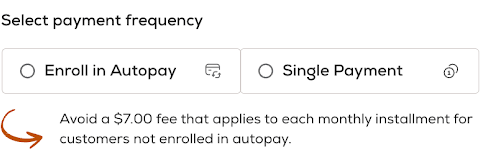

I was not able to modify my limits or deductibles to get cheaper business insurance. Three did not offer me the chance to pay annually either, only monthly. However, I had to sign up for autopay to avoid a $7 monthly fee.

Every time I review an insurance company, I use the same business details. Three’s quote was more expensive than quotes I’ve gotten in 2026 from Hiscox, Thimble and biBERK (another Berkshire Hathaway brand). It was roughly on par with my quote from Ergo Next.

That extra cost might be because Three’s coverage is more comprehensive. I was seeking general liability insurance alone from those other companies. My other quotes didn’t include professional liability coverage, for instance.

Methodology

Business insurance ratings methodology

NerdWallet rewards business insurance companies for reliability and good service. We calculate star ratings based on scores in about a dozen categories. These include:

Each company's financial strength.

How many complaints customers made relative to its market share.

Our editorial team routinely fact-checks and updates these data points. We also adjust our scoring on an ongoing basis. This helps our star ratings reflect changing industry norms. For instance, in 2026, we began evaluating how easy insurers make it to add an additional insured.

Our ratings are a guide. But insurance policy details and prices can vary widely. We encourage you to shop around and compare several insurance quotes. NerdWallet does not receive compensation for any reviews. Read our editorial guidelines.

Insurer complaints methodology

One key factor in our star ratings is how many complaints insurance companies get. Here's how we arrive at that score.

Disappointed customers can file a complaint with their state's insurance department. The National Association of Insurance Commissioners (NAIC) collects, analyzes and groups complaints by business line and insurance company every year. A business line is a specific type of coverage, like workers’ comp.

Then, the NAIC calculates a complaint ratio for each company. It divides the company's share of complaints by its share of total premiums for each line of business. It then adds these ratio values to their official complaint index.

A complaint ratio of 1 means a company received about the expected number of complaints relative to its size.

A ratio of 2 means it received twice as many complaints as expected.

A ratio of 0 means it received half as many complaints as expected.

NerdWallet obtains the raw NAIC data every year. We aggregate results at the company level and fact-check these results. Then we calculate a three-year average of each insurer's complaint ratio and convert it to a score for our star ratings.

Business insurance star ratings consider complaints about two lines of business: commercial liability and commercial property. We analyze complaint data on commercial auto and workers' comp policies too. But we don't currently incorporate these into our ratings since they're less universal.

Why trust NerdWallet

Why trust NerdWallet